Chances are your financial habits began to take shape at an early age. According to a study published by the Money Advice Service and behavioral experts at Cambridge University, “By the age of seven most children have grasped how to recognize the value of money.” The study goes on to highlight the power that parents possess to shape the money habits of their children, even claiming that many of these behaviors are taken into adulthood.

Table of Contents

Behavioral Finance: Where Money and Psychology Meet

Some financial experts think of money as a relationship – complicated, maddening, motivating, and constantly evolving. Here at Momentum Wealth, we believe that within our financial decisions is a degree of emotion. There is even an entire discipline devoted to how our emotions affect our financial decisions. It’s called behavioral finance.

Behavioral finance is the area of study focused on how psychological influences can affect market outcomes. Simply put, people are not always rational when making financial decisions – emotion and bias, even childhood subconscious and conscious behaviors come into play. Examples of emotionally driven financial behaviors are all around us, especially in the investment markets.

Breaking Habits to Create Financial Success

But what if you didn’t grow up with the best money-management role model? Are some people doomed from the start? Like many things in life, with a little will power and a lot of guidance, you can obviously break bad habits and improve your financial relationship.

Ultimately, being aware of early positive and negative influences can help our advisors understand risk tolerance and comfort level. Momentum Wealth offers a risk assessment questionnaire to better understand a client’s financial behavior and psychological influences. Results help determine investment strategies based on tolerance to risk. Often times, these assessments even bring to light behaviors unknown to the client.

How to Allocate Assets by Age

So now that we’ve tapped into our deep-rooted relationship with money, how do we create financial success? What does our asset allocation look like at each stage of life? We break this down into three significant financial phases: starters, spenders, and savers.

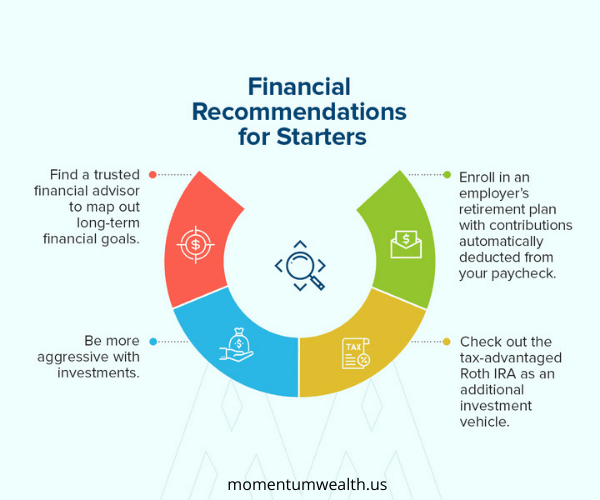

Starters

Overview: Momentum Wealth identifies this group as “Up-and-Comers.” People in their early 20’s just getting started with life. A starter is beginning his/her career, recently out of college, and saving to buy a house. Generally speaking, starters have more time to profit from investments before retiring. For this reason, many starters can be more aggressive with investments.

Financial Recommendations:

- Enroll in an employer’s retirement plan with contributions automatically deducted from your paycheck.

- Check out the tax-advantaged Roth IRA as an additional investment vehicle.

- Be more aggressive with investments.

- Find a trusted financial advisor to map out long-term financial goals.

Savers

Overview: This group ranges from 35-55 in age. Savers are in their peak earning years. Most likely, savers have earned a few raises and they are compounding savings and investments set up in their early 30s. Retirement is closer. During this phase, we advise pulling back on risk levels, while keeping in mind the end goal – retirement.

Financial Recommendations:

- Invest the maximum amount per year in a 401(k).

- Increase savings rate.

- Be prepared for unexpected life events.

- Nail down life and disability insurance.

- Consider setting up a 529 College Savings Plan.

- Ease up on super aggressive investments.

- Begin thinking about your exact retirement age. This will affect how much money is needed, and when.

Spenders

Overview: Momentum Wealth classifies this age group as 55 and up. Years of investing have compounded, allowing for a steady cash flow. We recommend dialing back on aggressive stock funds to reduce financial risk.

Financial Recommendations:

- Finalize estate plan (will, living will, and healthcare power of attorney).

- Study options for taking money out of company retirement plans.

- Review income streams and reallocate investments based on income needed.

Ultimately, the most important thing to remember: Create a financial plan and stick with it. Momentum Wealth suggests saving and investing as early as possible. Adding any amount to retirement savings is better than nothing. How you invest each decade will be determined by your savings and financial behavior. A solid financial advisor can help with overall goals and strategies for where you want to be in the future while keeping in mind how much risk you can tolerate.

Fill out a form or call Momentum Wealth directly. We will be there to advise you every step of the way.

The information in this article is for general informational and educational purposes only, and should not be construed as investment, tax, or other financial planning advice.