Whether it’s products, services, revenues, expenses — when it comes to owning and operating a small business, they all demand your attention. And it can become easy to forget about less immediate matters, such as employee benefits and savings goals.

Personal, business, retirement — savings have a tendency to take a back burner as we focus on building a lasting business. Deciding if, when, and how to make savings a priority for yourself and your employees is an important milestone in the growth of a small business.

A common misconception is that retirement savings plans, in general, are simply too expensive. Many entrepreneurs assume their business couldn’t possibly be large enough to take advantage of the plans that are out there. However, it’s actually quite a simple process to set up a retirement savings plan, and there are even a number of them that are designed specifically for small business owners like yourself.

The purpose of this guide is to help you find a balance between running your business, saving for retirement, and offering employee benefits that help them save for theirs.

Striking a Balance

Striking a balance between growing your business and saving funds for yourself and/or employees is not easy. We find that the best way to start is by looking at the bigger picture of where you want to be 10-20 years from now.

If your business is highly successful and you have the opportunity to sell it, you might have a liquidity moment that can fund your retirement. However, the reality is that most small businesses can’t operate without their owner and therefore can’t really be sold — or if they can, it’s typically not for a high multiplier.

Consider a CPA who has relationships with 100 clients and decides to retire. Someone could purchase their client lists and namesakes, but that CPA would likely only profit 3x their annual revenue from that. Studies have shown that people should save 18x their yearly pay — so 3x realistically won’t be getting that CPA very far.

That said, as the business owner, you have the responsibility to divert some of your business’s income into savings in order to hedge against a similar situation for yourself.

Let’s look at a few ways small business owners can successfully offer and manage – employee benefits and savings plans. We’ll start small with options that make sense for the business owner alone, and we’ll progress into plans that are better suited for those with employees.

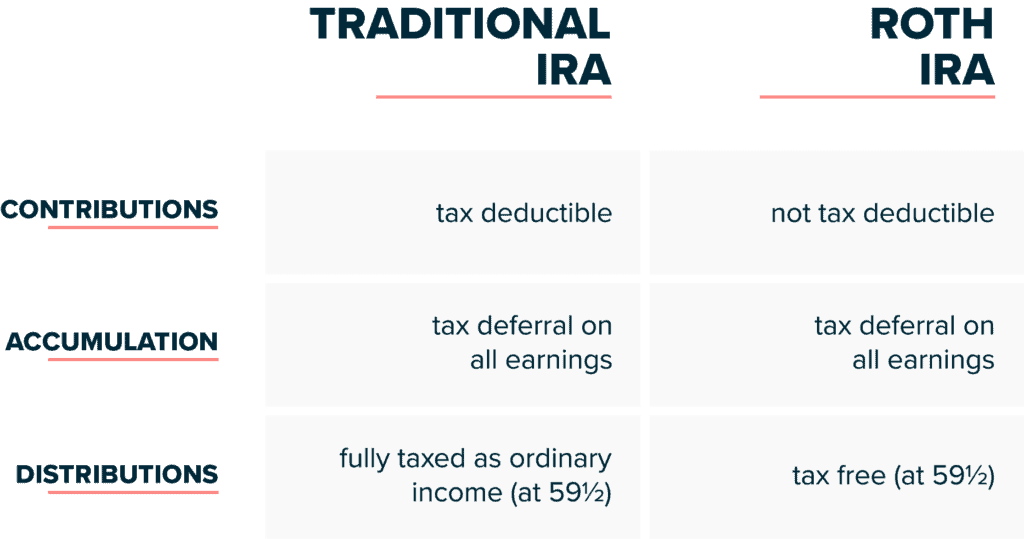

IRA (Traditional or Roth)

The first option we’ll look at is an IRA. It’s one of the most popular retirement savings options and comes in two flavors: traditional and Roth. Depending on your income level, this option may or may not be available to you.

Income limits are important to note when considering traditional or Roth IRAs because if you make too much money, then your ability to contribute could be affected.

For instance, if you file taxes as a single person, and your Modified Adjusted Gross Income (MAGI) is greater than $137,000, you won’t be able to contribute to a Roth. You can find all the updated income limits on the IRS website.

If you’re self-employed and don’t have access to another employer-sponsored retirement plan, it’s possible that you could contribute to a traditional IRA and get a tax deduction regardless of income. An advisor can help you figure out your eligibility based on your specific situation.

With a Roth IRA, there’s no way to get around the income limits — even if you don’t have any other type of employer-sponsored plan. The Roth is funded with after-tax dollars, so there aren’t any immediate tax deductions for contributions. Instead, the tax benefit of a Roth is realized in the future when you can take tax-free distributions from the account.

So what are your options if your income is too high for an IRA?

Solo 401(k)

One popular option among high-earning self-employed individuals is the Solo 401(k) — also known as the Solo K. It should be no surprise that this one’s also meant for those with no full-time employees.

A Solo 401(k) operates similarly to a 401(k) that large employers might offer in that you can make contributions as an employee and match them as the employer. Since you are both, they are, of course, all your contributions.

You can also add a profit share contribution that can push the annual contribution limits as high as $63,500. This can only be done when you have no employees — the exception being a spouse that also draws income from the business.

You will definitely want to work with an advisor to help navigate the filing, regulatory, and contribution rules associated with this one.

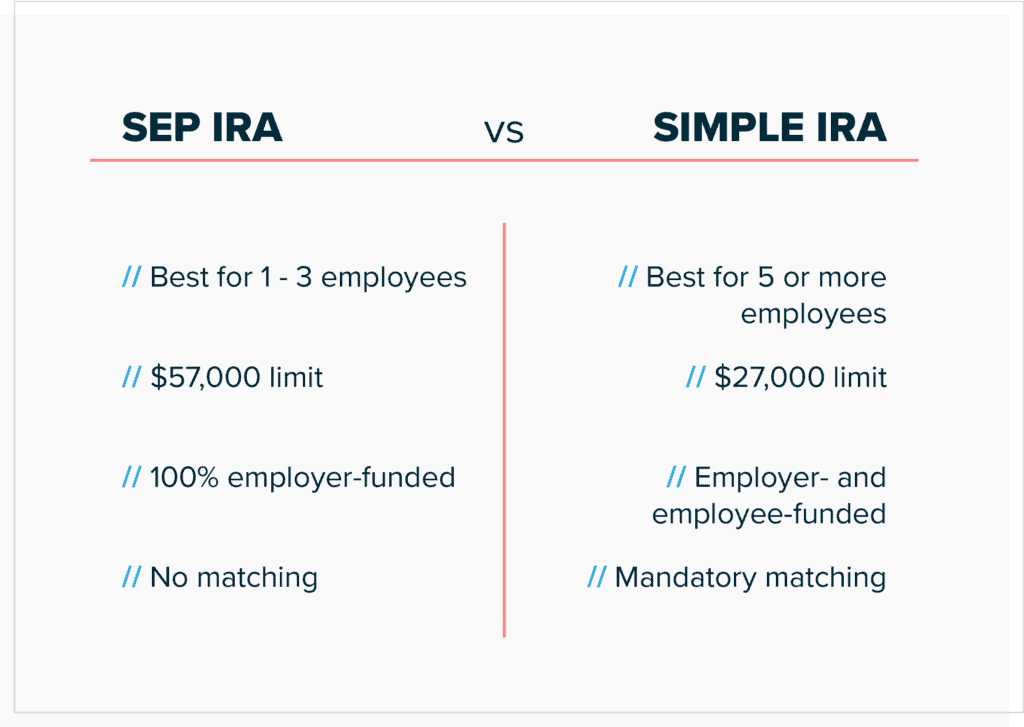

Simplified Employee Pension (SEP)

Once your business has reached the point where you can reasonably offer employee benefits, you have a few options to consider. The first of these is called a Simplified Employee Pension, also known as a SEP IRA.

Knowing which of these options is right for you starts with the size of your workforce.

The SEP is ideal for sole proprietors, single member LLCs, partnerships, and family-owned/operated businesses — basically as long as the workforce is either small, seasonal, or the only employees are also the owners.

Contribution limits are high and there are minimal filing requirements. Below are some additional features of a SEP IRA:

- Flexible contribution limits up to $54,000.

- Traditional IRA contributions can be made alongside SEP IRA contributions.

- Plans can be discontinued at any time, a major benefit given the volatility of early-stage small businesses.

- SEPs can be set up with an advisor to enhance portfolio construction and management. Working with an advisor provides the additional benefit of access to other financial planning services as well.

Now as we see, a SEP IRA only works for small numbers of employees or for the owner-operator alone. If you have full-time and/or permanent employees, then we need to explore a few other options.

Employees + Savings

You have to remember that this type of saving through payroll deduction into tax-deferred accounts is likely the only way most of your employees are saving for their futures. As such, it’s important for you to encourage them to take advantage of the employee benefits and savings programs you’re offering.

Furthermore, especially in the early stages of contributing, employer matches are often the only way employees see meaningful growth in their accounts.

Since we know schools don’t delve nearly far enough into the personal finance arena, having the option for workplace savings, as well as meaningful discussions around them, is a huge opportunity for employees.

This can have a profound impact on the way employees understand the connection between what they are doing right now and their future retirement. And that’s good for both your employee and your business.

Let’s look at some of the options you have for setting up your employee benefit offerings.

SIMPLE IRA

The SIMPLE IRA is, as its name would imply, pretty simple. It stands for Savings Incentive Match Plan for Employees, and it’s easy to set up and easy to manage. The most overlooked benefit of a SIMPLE IRA is that, if set up correctly, it offers employees a one-on-one relationship with an advisor that they’d otherwise most likely not have.

Other features include:

- Higher contribution limits: Participants can contribute more than with a traditional IRA, and employer matching or contributions are required.

- Tax benefits: Employer contributions qualify as a tax-deductible business expense.

- Affordable cost & flexible pricing.

- Easy plan design: No complex IRS reports to complete and no annual nondiscrimination testing required.

While there are many options and many ways to implement the various workplace savings plans available, there are some things to be aware of as far as cost is concerned.

What to look out for with SEP + SIMPLE IRAs:

Most SEPs and SIMPLEs are established using mutual fund companies directly, and by default, usually have commissions built into the share class. This means that every contribution is surcharged a commission. These are usually much higher than when working with an advisor who can use different share classes and remove any such surcharge.

Working with an advisor to set up and manage SEP or SIMPLE IRAs often means that the relationship between advisor and business owner also extends to the employees. Now your employees have access to benefits and planning services that they might not have otherwise had.

And when employees are financially fit, they tend to enjoy their jobs more, focus more, and be more productive at work. Again — a win for both sides.

Safe Harbor 401(k)

The Safe Harbor 401(k) is one of the most overlooked options for small businesses. It follows the standard 401(k) rules and contribution limits, except that you can avoid what’s called “nondiscrimination testing.”

This means that highly compensated employees (HCEs) are able to contribute the same amounts as other employees. With a Safe Harbor plan, you have to help your employees save by contributing to their 401(k) plans. You have a few options as far as how to contribute, but all your employee contributions are tax-deductible.

In a standard 401(k), the plan sponsor has to monitor the percentage of HCEs, and if the plan becomes too top-heavy, contributions have to be refunded. See this 401(k) fix-it guide from the IRS for more information.

The Bottom Line

There are plenty of options for employers to take advantage of employee benefits in order to build savings for themselves. If you own a business, I highly encourage reaching out to an expert on this topic. They can provide clear guidance on properly executing one of the aforementioned plans.

A few things to keep in mind as you go through the process, regardless of who you work with:

- Pay attention to the costs, especially the less obvious ones involved.

- Make sure the advisory firm you engage with is committed to educating you and your employees.

- Avoid commissioned environments if possible.

We’ve worked with many entrepreneurs on this exact initiative, helping to guide their small businesses into this exciting stage. You can fill out a form or give us a call, and we’ll be there every step of the way for yours.