Social Security is our greatest source of government-guaranteed, inflation-adjusted, lifetime income we’ll get in retirement. But it sure isn’t easy to navigate. There’s tons of information out there, but a Google search will quickly show you how contradictory, confusing, and outright wrong much of that information is.

For instance, did you know that Social Security has over 2,700 different claiming rules? Or that together those rules leave married couples with over 567 different potential filing strategies?

Once you realize the scope, it’s suddenly not so shocking that a whopping 96% of Social Security claimants fail to optimally make their claims. And the consequences of that are substantial — as in $3.4 trillion in lost potential income. The average loss per household comes out to be about $111,000 — all because of suboptimal claiming strategies.

The SSA isn’t much help either.

Even the Social Security Administration itself reports that bad Social Security advice has cost Americans $131 million. And they’re often the ones giving the bad advice in the first place!

Have no fear. Buried somewhere among all these options is the perfect plan for you and your life circumstances — the best way to file that maximizes your guaranteed income, protects your spouse’s income, and creates your most tax-optimized retirement paycheck.

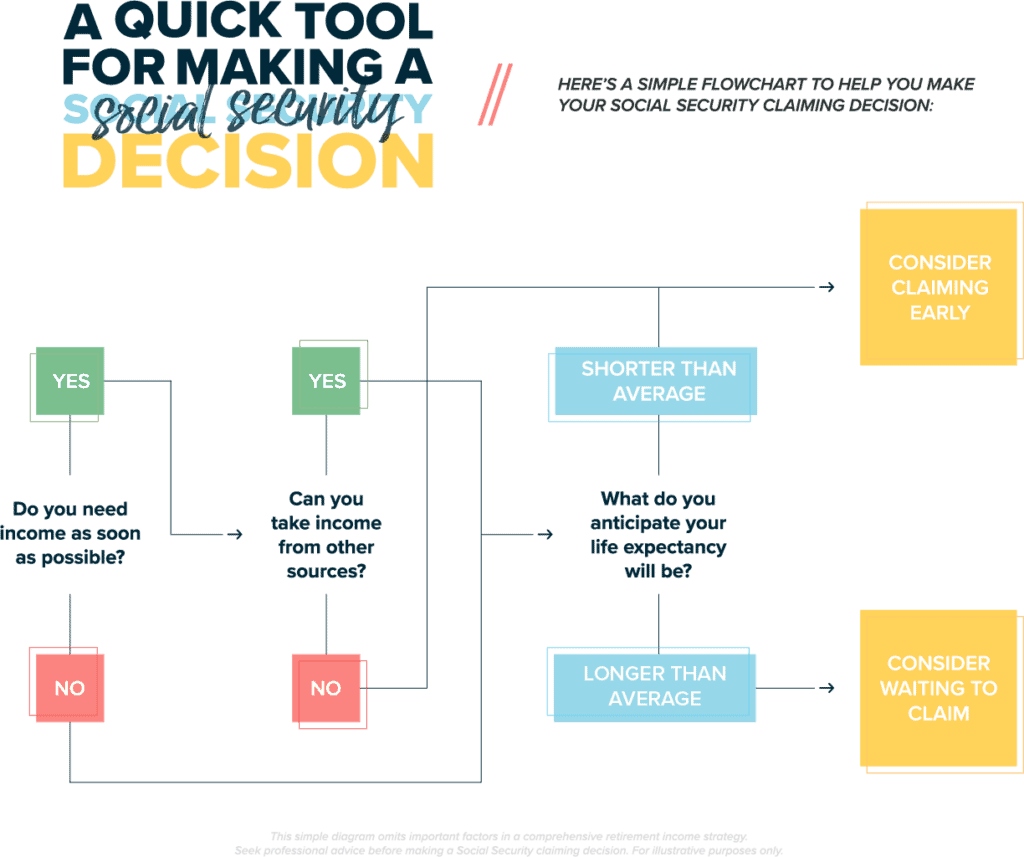

The purpose of this guide is to demystify the concept and inner workings of Social Security to put you in more control of your financial future. We’ll break down the most critical factors, as well as guide you through a simple flowchart to help you make your claiming decisions.

#1 Question: When should you claim Social Security?

When it comes down to it, the earlier you file, the less you’ll receive in benefits each month. And that’s the case for as long as you continue claiming.

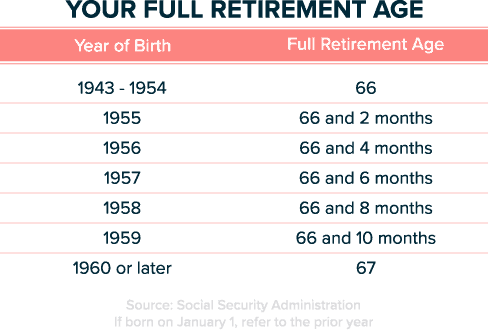

If you wait until you hit your Full Retirement Age (FRA), you’ll be able to claim 100% of your benefit, but you can start collecting as early as age 62. See the chart below for what age is considered your FRA based on the year you were born.

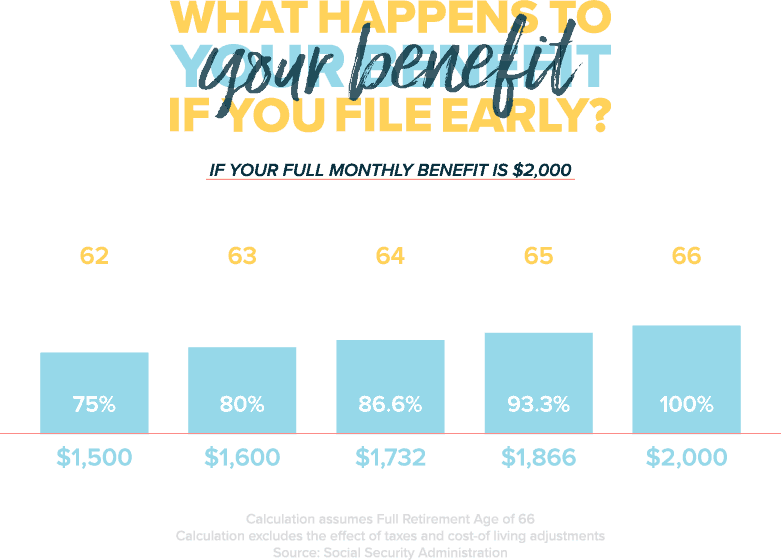

Let’s say your FRA is 66 years old, and your full monthly benefit is $2,000. If you sit tight and wait until you turn 66, you’ll receive 100% of that benefit amount. However, as you can see from the figure below, you’ll only see a percentage of those benefits if you file early and start collecting before reaching FRA.

Now, just because you’ll lose out on collecting the full benefit amount, filing early is can still be a smart move. It all depends on your individual situation, so let’s get into that.

Reasons to claim Social Security early (between ages 62-67)

Claiming early means you’ll collect checks for a longer time, but they won’t be for the full potential amount. In fact, for every year that you claim early, you’ll be giving up between 5% and 6.67% of your full benefit.

Even so, there are several common, legitimate reasons for choosing to claim Social Security early:

- Your spouse is a high-income earner, whose benefit can keep growing while you claim your own.

- You need income early on in retirement.

- Your life expectancy may be lower than average.

- You don’t want to withdraw from your retirement savings yet (and want them to keep growing at market rates).

Reasons to claim Social Security at your FRA (ages 66-67):

Waiting until you hit FRA to claim your Social Security means you’ll get 100% of the benefit amount. However, you’re technically allowed to keep collecting for a few more years after that. So claiming at age 66 or 67 means you forfeit the opportunity for your benefit to grow even more.

Here are three main reasons to claim Social Security at your FRA:

- You won’t lose out on any benefit amount to which you’re entitled.

- The Annual Earnings Limitation goes away, so you can keep working while still collecting your full benefit.

- You can still suspend your benefits at any time to allow them to start growing again.

What about waiting even longer to claim?

If none of those reasons apply or appeal to you, you can hold off on claiming Social Security. Once you turn 70 though, your benefits have grown as much possible, so there’s no longer a reason to delay.

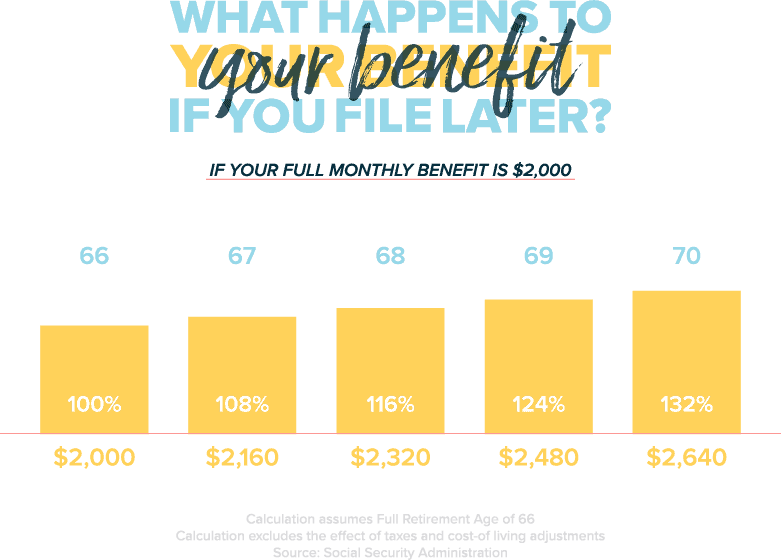

The figure below demonstrates your potential benefit amount if you wait to claim them.

As you can see, if you reach FRA but wait to claim your benefits, you’ll get to bring home a larger monthly percentage once you do claim them. It’s all about finding the balance that works for your needs and lifestyle.

Why choose one claiming strategy over another?

There are plenty of things to consider when weighing your options. We’ll break down four of the most important questions we ask clients when discussing Social Security and retirement income.

1. What other sources of retirement income do you have?

If you want to retire, but you’ll still have money coming in from other sources, you have the luxury of flexibility here.

For instance, you might have a guaranteed income stream from another source, such as an annuity. In that case, you could reasonably delay claiming Social Security until hitting Full Retirement Age or even later. Holding off on claiming those benefits would maximize the amount you’ll eventually receive.

On the other hand, you could look at it from the opposite perspective. Claiming Social Security as early as possible would give your investments more time to grow in the market.

Calculating your potential earnings depends on a number of variables best handled by professional software. As financial advisors, we’ve got the tools to help you run the numbers and analyze your options.

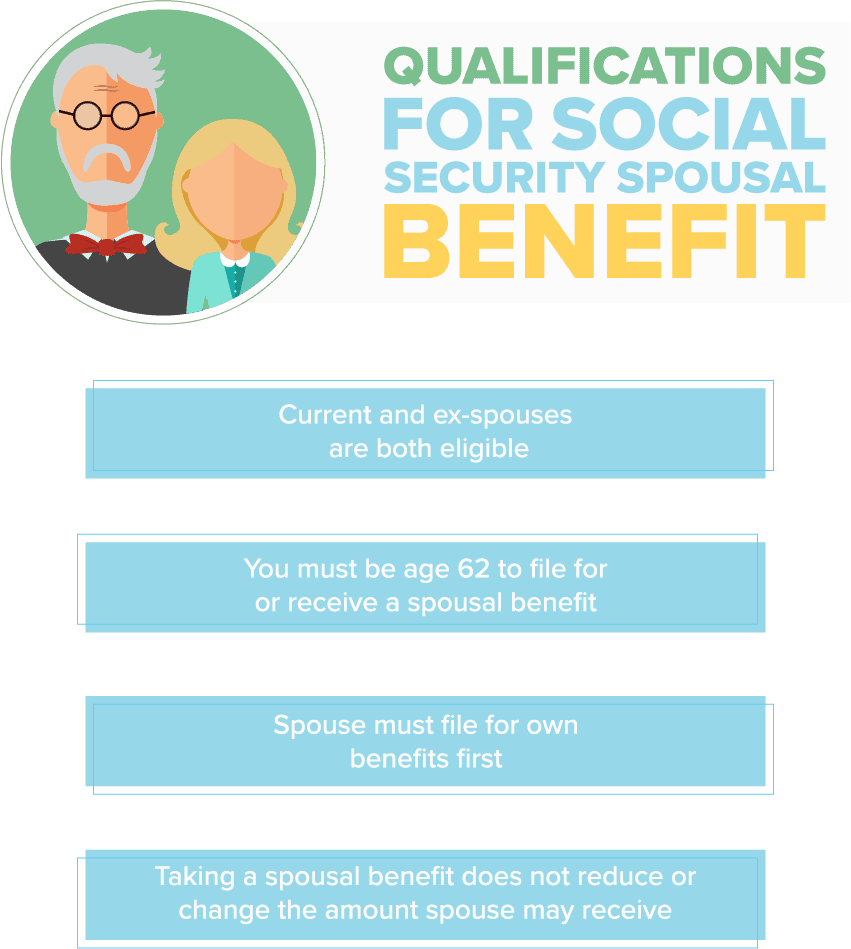

2. Are you married?

Married people have more options to consider since they can choose to claim on their own record or choose to claim on their spouse’s record (if they are eligible). You’ll want to consider both of your survivor benefits to ensure that a surviving spouse isn’t left without enough income.

There used to be a strategy called “file and suspend” that enabled married couples to simultaneously delay retirement credits while receiving spousal benefits. While that’s no longer allowed, there are still plenty of other advanced strategies out there. We recommend working with an advisor to navigate them and maximize your income now and in the future.

3. What are your expectations regarding family health history and longevity?

In theory, Social Security is designed to pay people the same total amount whether they collect early or late. However, that design is based on the assumption that people will live to their exact average expected age.

That’s why life expectancy is such a critical factor in your personal Social Security plan. If you expect to live longer than the break-even age, waiting as long as possible to claim means eventually receiving the largest benefit.

Of course, other variables come into play when determining the exact age at which you’ll maximize your lifetime benefits. Those include the amount of your benefit, your tax bracket, how your retirement portfolio is performing, etc.

It’s a complex calculation. That’s why we encourage you to both educate yourself and work closely with an advisor to strategize.

4. Will you work while claiming Social Security?

If you intend to work while claiming Social Security, you need to consider two additional factors: the Annual Earnings Limit (only affecting those under their Full Retirement Age) and taxes. More of your benefit becomes taxable if your overall income (including Social Security and income from other sources) is above certain annual thresholds.

So if you don’t feel like paying taxes on up to 85% of your Social Security income, I encourage you to get in touch. There are a number of strategies we can use to adjust your taxable income to reduce the taxes you pay.

How to think about creating your own Social Security strategy:

There are plenty of factors and extenuating circumstances that have an impact on constructing your ideal plan. We’ve covered a number of them, but we also want to encourage you to start simple.

That’s why we created this flowchart as a quick and simple tool to get your gears turning.

Caution: The wrong path can cost you thousands in lost income.

That’s no small number, and even though starting simple is a good start, this decision isn’t one to take lightly.

- Before anything else, take a step back and consider all the options available to you and your spouse.

- Talk to a professional about your retirement income plan. The keyword here is professional. Financial consultants are professionally trained to help with these decisions for a reason. Take advantage of their expertise for your benefit.

- If you’ve already filed but made a mistake (or think you’re better off with a different strategy), give us a call immediately. We may be able to help you “turn back the clock” on your benefits and still maximize your income.

We’ve brought up the importance of having professional guidance through this process. But let’s break down a few of the tangible benefits that come with getting a professional opinion.

The Deliverables

- Software that analyzes all 2,700+ Social Security rules, showing how to optimally claim yours to maximize income now and later

- Personalized analysis of all advanced claiming strategies, including 62/70, Start-Stop-Start, Claim and Grow, as well as limited opportunity loopholes you may not be aware of

- Tax-smart income plan that shows you exactly how to structure withdrawals from retirement accounts and Social Security to minimize taxes

The Bottom Line

Social Security is the furthest thing from “one size fits all.” But too many Americans are approaching it as such. And because of that, there’s so much money on the table that they’re simply allowing themselves to lose.

On average, recipients would receive 9% more income in their retirement if only they’d made the right financial moves combined with the right timing. We’ve got all the tools to help you do exactly that.

If you don’t want to look back on your retirement decisions with resentment and the feeling of “what-if?”, reach out to us today.

You can fill out a form or give us a call, and we’ll work with you to develop the best path forward.

The information in this article is for general informational and educational purposes only, and should not be construed as investment, tax, or other financial planning advice.