Whether you’re changing jobs or coming up on retirement, you’ve got some decisions to make regarding the money you’ve accrued in your old 401(k). When you leave your place of work, the retirement plan to which you’ve been contributing (unfortunately) doesn’t magically move for you.

If you’re lucky enough to have an employer plan, typically a 401(k), 403(b), or a 457, you want to hold onto as much of that money as possible.

An improper retirement plan rollover can cost you big-time — including surprise tax bills, IRS penalties, and missing out on potential future wealth.

But handle it the right way, and you’re protecting your money’s tax-deferred growth and positioning yourself to hit your current and future goals.

You typically have four main options — two of which maximize the control you have over your money. It’s important to take note of each path’s pros and cons, and know what to expect before making a decision on your approach.

We’ll start with the most obvious options first.

Option 1: Don’t Touch a Thing

Some employers allow their employees to leave their old 401(k) in place after they’re gone. That’s nice of them, but it’s not doing you any favors since you’ll have limited ex-employee services, and won’t be able to contribute any more funds.

Pros:

- You may have access to plan loans and qualify for federal creditor protection

- If you retire after age 55, you may not owe a 10% penalty on withdrawals

- You might qualify for a special tax break if you own considerable company stock

Cons:

- You’re left with a trail of old accounts that aren’t really doing anything for you

- Plan fees might increase without your knowledge

- You have limited withdrawal and investment options

- Your investments are probably not optimized for taxes or your overall financial goals

To put this into “action”, you only need to contact your plan administrator and ask them to leave your plan in place.

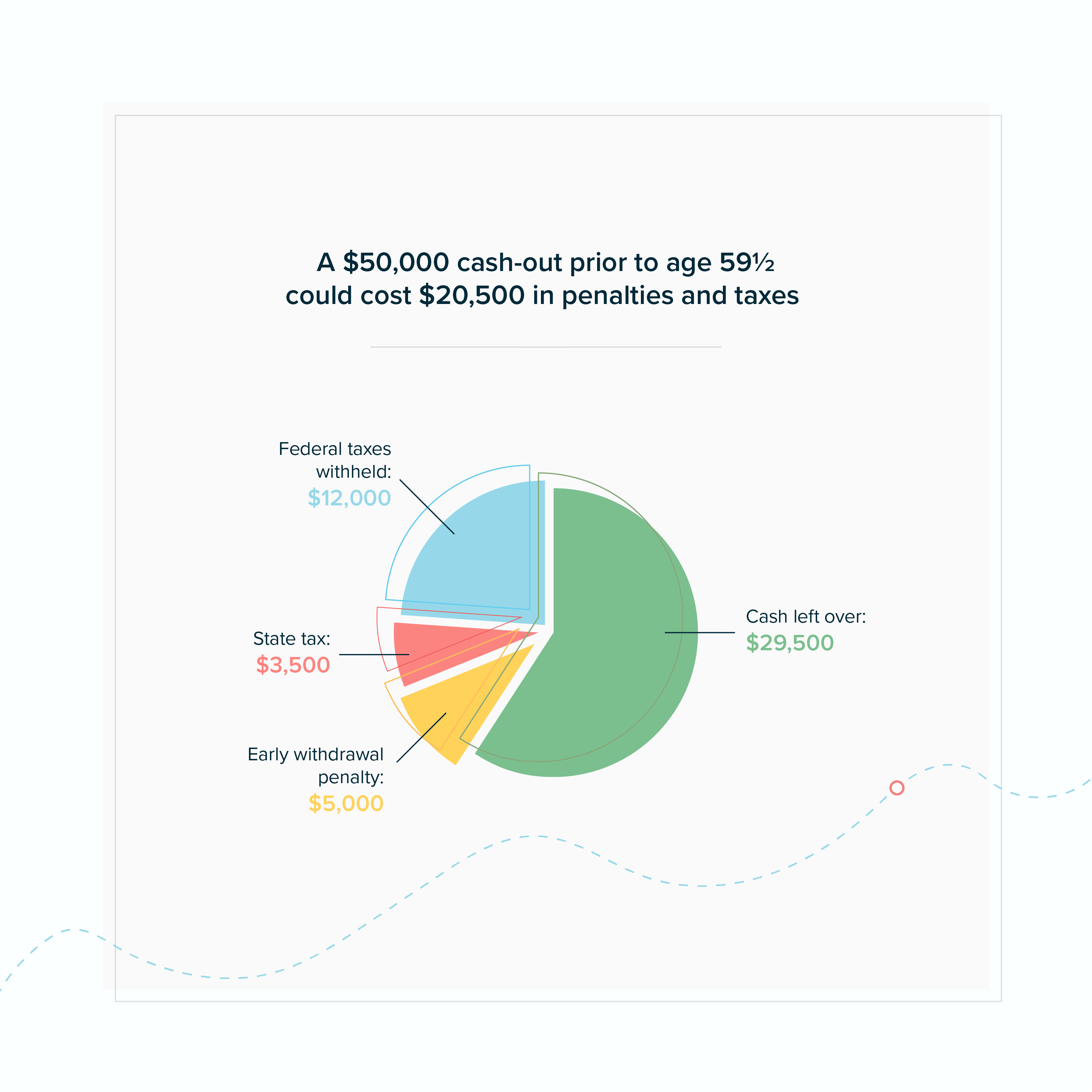

Option 2: Raid the Piggy Bank

This approach is the exact opposite of Option 1. It’s also pretty much the worst thing you could do because of the serious (and permanent) financial repercussions. Seriously, the only pro is that you’ll get immediate cash.

Cons:

- You’ll owe income taxes on the account value

- Your employer may automatically withhold 20% for taxes

- You’ll most likely owe penalties if you’re underage 59½

- Permanent damage to your long-term goals

Same action plan goes for this option — contact your plan administrator, but this time you’d ask them to liquidate the account and send you a check.

Option 3: Move Your Old 401(k) To Your New Employer

Similar to Option 1, whether you can do this or not is up to the individual employer. Some will let you simply transfer your balance from your old plan over to your new one. It’s worth asking your new employer because this scenario has its benefits. For instance…

Pros:

- All your employer plans will still be in one place

- You won’t pay taxes on the distribution if you transfer directly

- You’ll have the protections and benefits of the current plan

Cons:

- Your investment options will be limited to those offered by your new plan

- Many employers require a waiting period before you’re eligible to enroll in the new plan

If this is the move for you, get in touch with HR at your new employer and ask them to connect you with the plan administrator. If they allow this kind of transfer, the administrator will walk you through completing it.

Let’s look at the two different ways you can roll over your retirement plan into an IRA:

- Indirect IRA Rollover

- Direct IRA Rollover

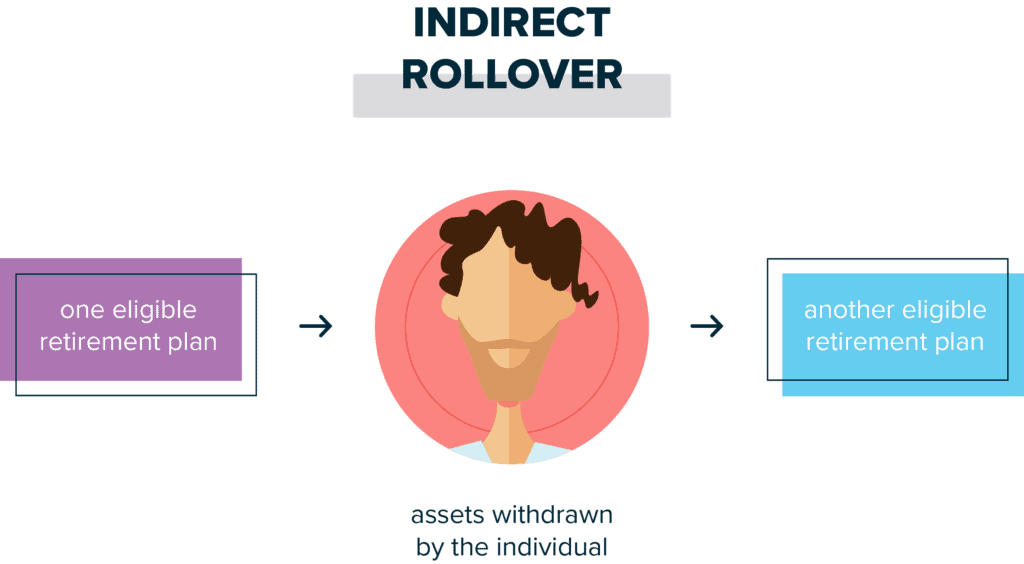

Option 4a: The Not-So-Simple Indirect IRA Rollover

The first of these options is basically a more convoluted way of achieving the same goal as the second. If you go this route, you essentially get a free 60-day loan between cashing out your old 401(k) and rolling that money over into an IRA. However, this is risky, and you’ll see why.

Pros:

- Immediate access to all that cash for 60 days

- Once the rollover is completed, you get all the benefits of an IRA, including:

- Access to lots of investment options

- Tax optimization strategies (e.g., Roth conversions, backdoor Roth IRAs, etc.)

- Investment optimization for your overall financial picture and long-term goals

Cons (Buckle up because there’s a bunch):

- It’s on you to remember to manually deposit your check into your IRA within those 60 days

- Taxes and potential penalties if you don’t complete the rollover within that time frame

- Indirect rollovers get reported to the IRS

- You risk making your retirement funds fully taxable forever

- You lose out on any potential market gains happening in your rollover window

- You’re limited to only one indirect rollover per calendar year (no matter how many accounts you have)

- Your employer may still withhold 20% for taxes (for which you’d have to make up from other funds)

- In most cases, you’ll be hit with a penalty for withdrawing from an IRA before age 59½

- Assets in employer retirement plans typically have greater protection from creditors than those in an IRA

You can technically complete this type of rollover on your own by having your former plan administrator liquidate your account and send you a check. You would then send that check to your new IRS custodian and have it deposited within 60 days.

BUT this is by far the rollover that most often leads to mistakes and IRS penalties, so you should consider working with an advisor to guide and assist.

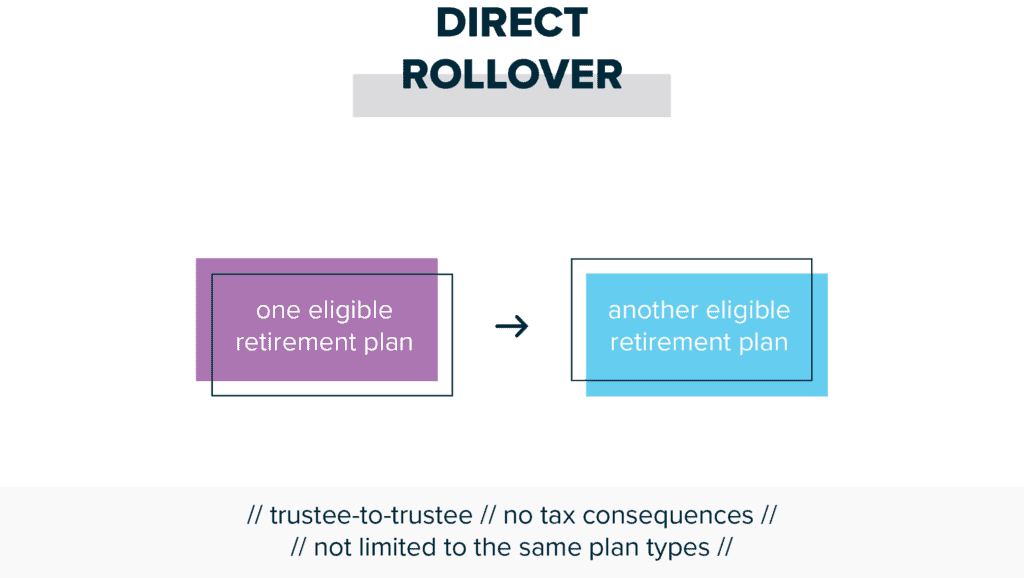

Option 4b: Direct Rollover to IRA

This route comes with some paperwork and careful consideration of the right kind of IRA, but it’s the smartest way to avoid nasty mistakes and maintain maximum control over your finances. This move comes with all the pros of an indirect rollover, plus…

Pros:

- By never taking “custody” of the money, you avoid all potential IRS penalties

- You won’t owe taxes on the transfer

- Your employer won’t withhold any amount from the balance for taxes

Cons:

Though you’ll run into some of the same cons as an indirect rollover, you avoid any issues having to do with accidental penalties, unexpected fees, or employer-withheld taxes.

Plus, if you’re working with an advisor, they’re with you every step of the way to get through the paperwork, evaluate IRAs to pick the right one, and keep you pointed in the right direction for your goals.

As you can see, different situations call for different approaches, and there’s a lot to think about when it’s time to decide what to do with your money. The #1 mistake people make, though, is doing absolutely nothing. If you’re not sure where to start, or this made you think of a thousand more questions, we’re here to help.

You can fill out a form here to connect with us, or just give us a call directly. We look forward to hearing from you and working together to reach your financial goals.

The information in this article is for general informational and educational purposes only, and should not be construed as investment, tax, or other financial planning advice.